accumulated earnings tax irs

The purpose of the tax. According to the IRS anything.

Chapter 12 Dividend Policy Learning Goals 1 Understand

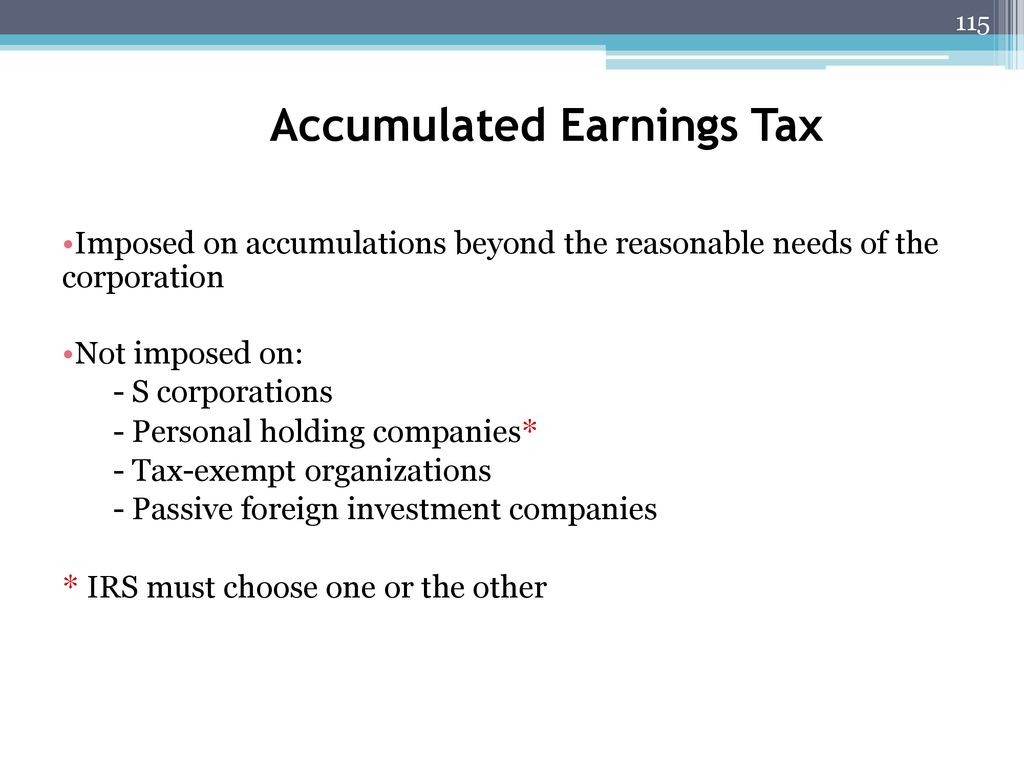

The AET is a penalty tax imposed on corporations for unreasonably accumulating earnings.

. To avoid having to pay for accumulated earnings tax Company A has to distribute at least 100000 of net income as dividends. The accumulated earnings tax imposed by section 531 shall apply to every corporation other than those described in subsection b formed or availed of for the purpose of avoiding the income tax with respect to its shareholders or the shareholders of any other corporation by permitting earnings and profits to accumulate instead of being divided or distributed. The purpose of accumulated earning tax is to discourage the accumulation of profits if the purpose of such accumulation is to enable shareholders to avoid paying taxes on those profits by not paying them dividends.

The threshold is 25000 without accumulated earning tax. In light of recent IRS enforcement efforts corporations should take action to defend against the potential imposition of the accumulated earnings tax. 150000 200000 - 100000 250000.

If a C corporation retains earnings doesnt distribute them to shareholders above a certain amount an amount which the IRS concludes is beyond the reasonable needs of the business the corporation may be assessed tax penalty called the accumulated earnings tax IRC section 531 equal to 20 percent 15 prior. In addition to other taxes imposed by this chapter there is hereby imposed for each taxable year on the accumulated taxable income as defined in section 535 of each corporation described in section 532 an accumulated earnings tax equal to 20 percent of the accumulated taxable income. There is a certain level in which the number of earnings of C corporations can get.

A corporation can accumulate its earnings for a possible expansion or other bona fide business reasons. IRC Section 535c. Accumulated Earnings Tax can be reduced by reducing Accumulated Taxable Income.

He accumulated earnings tax AET is imposed by Internal Revenue Code IRC section 531 on C corporations formed or availed of for the purpose of avoiding the imposi-tion of income tax on their shareholders by permitting earnings and profits to be accumulated instead of being distrib-uted. Publicly held corporations with many. Also called the accumulated profits tax it is applied when tax authorities determine the cash on hand to be an excessively high amount.

Breaking Down Accumulated Earnings Tax. A corporation determines this amount by adjusting its taxable income for economic items to better reflect how much cash it has available to make dividend distributions. The accumulated earnings tax also called the accumulated profits tax is a tax on abnormally high.

If a corporation pursues an earnings accumulation strategy where the accumulation is to avoid the tax on dividends rather than having a business purpose then IRC 532 provides an accumulated earnings tax that can be assessed on accumulated earnings with no clear business purpose. The accumulated earnings tax can be a hidden penalty tax on highly profitable corporations that allow their earnings to accumulate without paying adequate or any dividends to their shareholders. The accumulated earnings tax is a charge levied on a companys retained earnings.

An accumulated earnings tax is a tax imposed by the federal government on corporations with retained earnings deemed to be unreasonable or unnecessary. The tax is in addition to the regular corporate income tax and is assessed by the IRS typically during an IRS audit. The accumulated earnings tax equals 396 percent of accumulated taxable income and is in addition to the regular corporate tax.

How Does Accumulated Earnings Tax Work. The tax rate on accumulated earnings is 20 the maximum rate at which they would be taxed if distributed. Code 531 - Imposition of accumulated earnings tax.

As a practical matter the tax is col-. What is the Accumulated Earnings Tax. IRC 532 a states that the accumulated earnings tax imposed by IRC 531 shall apply to every corporation other than those described in subsection IRC 532b formed or availed of for the purpose of avoiding the income tax with respect to its shareholders or the shareholders of any other corporation by permitting earnings and profits to accumulate instead of being.

The Accumulated Earnings Tax is computed by multiplying the Accumulated Taxable Income IRC Section 535 by 20. The Accumulated Earnings Tax is more like a penalty since it is assessed by the IRS often years after the income tax return was filed. Keep in mind that this is not a self-imposed tax.

When the revenues or profits are above this level the firm will be subjected to accumulated earnings tax if they do not distribute the dividends to shareholders. The base for the accumulated earnings penalty is accumulated taxable income. However if a corporation allows earnings to accumulate beyond the reasonable needs of the business it may be subject to.

When the amount of retained earnings in a company exceed a certain amount and is not distributed as dividends to shareholders the company is taxed on the accumulated income The US Internal Revenue Service allows for companies to accumulate profits of up to 250000 without paying tax since it believes that an amount exceeding this goes over the reasonable. The point of this tax is to encourage companies to issue dividends to their shareholders rather than sit on the earnings which ironically often leads to the shareholders paying taxes on the dividend income. As provided in section 535 a and 1535-1 the accumulated earnings credit provided by section 535 c reduces taxable income in computing accumulated taxable income.

An IRS review of a business can impose it. In the case of a corporation not a mere holding or investment company the accumulated earnings credit is determined as provided in paragraph b of this section and in the case of a holding or. Accumulated Earnings Tax.

1 Accumulated taxable income is taxable income modified by adjustments in 535 b and as reduced by the dividends paid deduction under 561 and the accumulated earnings tax credit under 535 c.

Earnings And Profits Computation Case Study

Simple Strategies For Avoiding Accumulated Earnings Tax Tax Professionals Member Article By Mytaxdog

Irs Schedule M 1 And M 2 1120 F Form Pdffiller

2

2

2

Earnings And Profits Computation Case Study

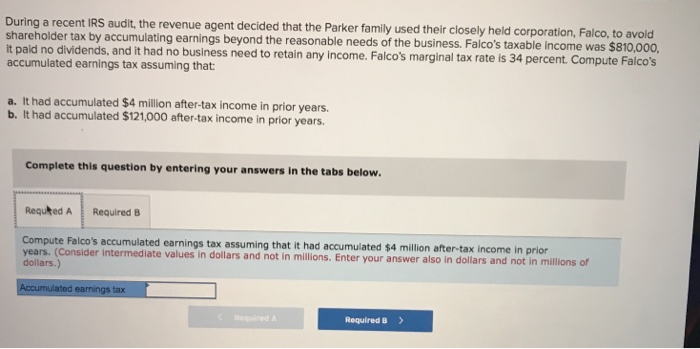

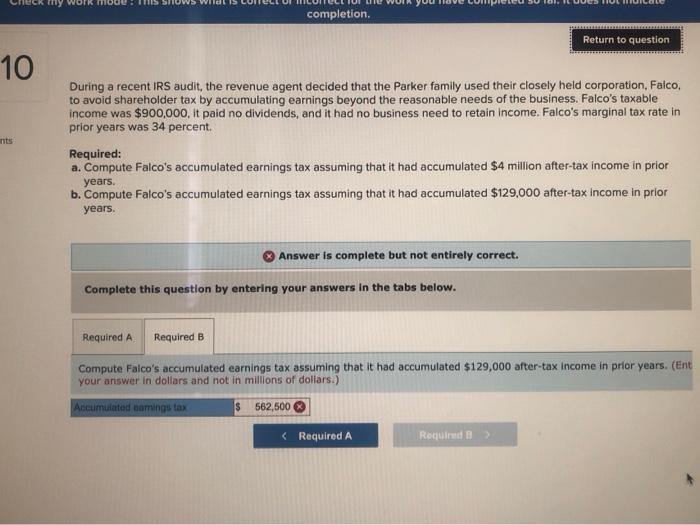

Solved During A Recent Irs Audit The Revenue Agent Decided Chegg Com

2

How Corporations May Run Afoul Of The Accumulated Earnings Tax A Section 1202 Planning Brief Frost Brown Todd Full Service Law Firm

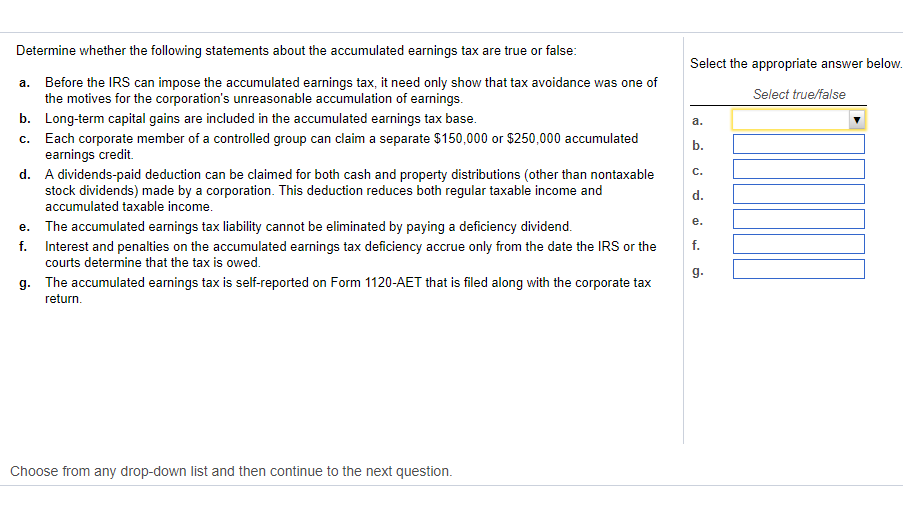

Solved Determine Whether The Following Statements About The Chegg Com

Irs Use Of Accumulated Earnings Tax May Increase

Bardahl Formula Calculator Defend Against Accumulated Earnings Tax

Corporate Tax Copyright Ppt Download

Demystifying Irc Section 965 Math The Cpa Journal

Understanding The Accumulated Earnings Tax Before Switching To A C Corporation In 2019

How To Calculate The Accumulated Earnings Tax For Corporations Universal Cpa Review

Solved Completion Return To Question 10 During A Recent Irs Chegg Com

Strategies For Avoiding The Accumulated Earnings Tax Krd Ltd